Director/shareholders of UK limited companies tend to reward themselves will a small salary and a dividend. The recommended system for 2024/25 is set out here.

However, in order to get the calculations absolutely right you need to know how much profit the company has, and you probably won’t know that until after the year end accounts have been done. So, part way through a trading year we don’t call these figures “dividends” and we suggest that you take “drawings” in the expectation that a dividend can be declared.

As a rule of thumb you can calculate your drawings using this method. It ignores some fine detail of accounting, but it will get you through to the year end.

Set up a separate company bank account for your company to hold its tax reserve. That’s for corporation tax and (if you’re VAT registered it’s also) for VAT. One savings account is enough.

When a client pays you, put aside 20% of that fee as a provision for corporation tax. Also put aside all of the VAT you charged on that invoice. OK, that ignores allowable expenses and things, and it will be a little too much, but it’s better to have too much tax reserve than too little.

What are you left with, net of corporation tax and net of VAT? Maybe knock off something for expenses as well. Then you have some idea of what the company can afford from its “distributable” profits.

Use that notional figure, and that’s the maximum drawings you can take.

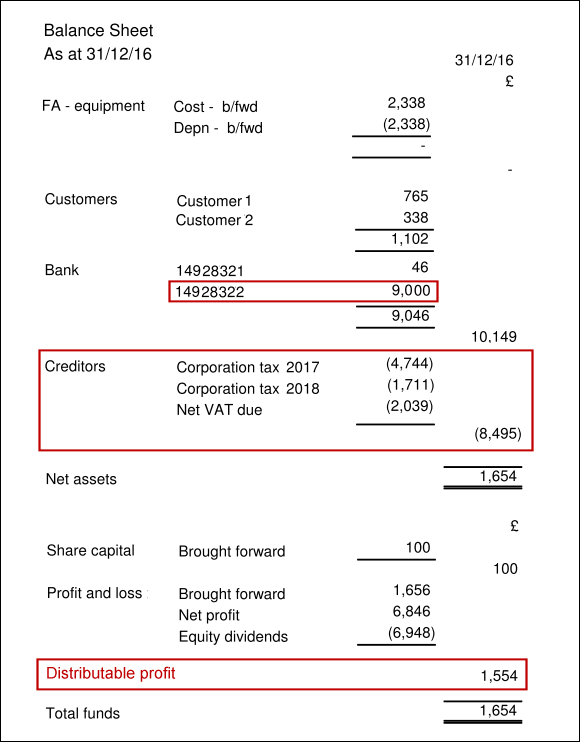

At the end of each quarter, when the bookkeeping reports (and the VAT reports) are done, have a look at your balance sheet. It shows you a forecast of the corporation tax (and the VAT), along with the bank balances on that quarter end date.

In the example above, the tax reserve (in bank account number 2) is £9,000 and that’s £505 more than the total tax forecast of £8,495. This is a good thing.

To the extent that your savings account balance (on the quarter end date) exceeds your creditors balance (on the quarter end date), then you have over provided for tax. If you want to, you can take that excess and move it back to the current account to employ the funds usefully in the business. Or if it’s the other way around, please take steps to restore your tax reserve to its rightful level.

Over time, you might want to adjust that 20% rule down to 19% or 18%. It will take several quarters before you get a feel for what is the right percentage in the case of your own company, and it will depend on having like for like activity each quarter. You’ll know when you hit the right percentage when, every quarter, the excess/deficit on the savings account is consistently small enough to make little difference.

As long as your name does not already appear under “creditors”, then the balance sheet may also show you what the maximum available amount of “distributable” profit is. Assuming that a director’s name does not feature on the balance sheet, then the example above shows that £1,554 is available. That’s just above the bottom line “total funds” figure, and it’s what the company is worth once you ignore the “share capital” line.

If your name is in the “creditors” block then a bit more arithmetic is needed. Firstly, don’t be in that territory on the quarter end date, and secondly, ask your accountant to tell you where you actually stand.

Please do not draw out more than the company can afford. If you do, then HMRC will seek retribution, and they will seek seriously penal levels of tax. We will tell you every quarter when you’re in the danger zone.