Proactive is no longer accepting new clients

Category: Proactive

The Universal Problem Solving Technique

Wouldn’t it be nice if you could have a Universal Problem Solving Technique which could help you solve any problem?

Yes, we think so too.

So at Proactive Towers in 2005, we set about building a Universal Problem Solving Technique (UPST). It’s a constantly evolving set of documents and we realise that our version of the UPST is not the same one that everybody needs. It’s simply the UPST that works best for us.

There are probably as many UPSTs as there are businesses on the planet. That shouldn’t stop you from building and using your own. It improves efficiency and it helps speed up your processes. That leads to increased profits.

Here are a few insights into ours to help you get started.

The Universal Problem Solving Technique starts with a set of approximately 10 flowcharts, and is backed up by a knowledge base which runs to over 500 articles. It didn’t all happen in one day!

Decades later, various bits of this massive edifice are tweaked on a regular basis. The world changes, life changes, and our UPST changes. Regular work does not require a check of the core UPST. The core is used when some delicate matter needs attention. It’s the lubricant which reduces friction when dealing with customers, suppliers, staff and assets.

- How do we respond to (our customer) Fred?

- How do we respond to (our supplier) Wilma?

- How do we handle (our employee) Barney?

- How do we handle the failure of (our equipment) Betty’s laptop?

Imagine that you own an old second hand car. At some point you’re going to dispose of it, because the repeated cost of maintenance and repairs outweighs the utility of keeping it. The UPST addresses that. It’s both an art and a science, and we’re trying to build a systematic and useful tool which minimises wasted time and money. Is that something that interests you?

A sample of the flowcharts was presented at the DDD North conference in 2022. It starts with a “Pioneer” flowchart which determines the route to be taken through the UPST. That quickly leads to a further flowchart related directly to the problem at hand. The “business” flowchart is illustrated below. This particular flowchart is the one which applies when you are the proprietor of the business. There are different flowcharts when the business in question is not your own.

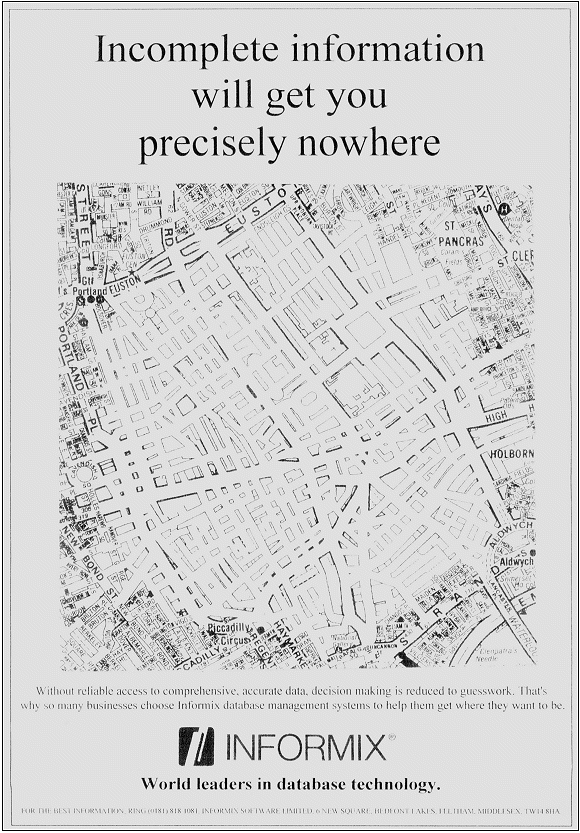

In business, having the right information to hand helps with decision making. Hence this flowchart starts by referring you to a 1988 advert by a company called Informix. In the days before the web (and back when scanners were low quality) we saw this in a newspaper and kept a copy. It shows a black and white street map of central London, with half of the road names missing, and boldly proclaims:

Incomplete information will get you precisely nowhere

In order to even start addressing your problem you may need to ask your counterpart to provide more information. We sometimes end up having to do a bit of forensic accounting, and we sometimes dismiss a client. It all depends on how much information we can gather.

It’s also important to discuss the perennial “why” question. The sort of thing that the average 3 year old will repeatedly ask. All the staff at Proactive Towers are familiar with this story.

| The perennial “why” question

The ultimate answer to a series of “why” questions is always: “sub-atomic particle physics” After a few authentic questions and responses, the answer eventually becomes “sub-atomic particle physics”. That same answer is then given repeatedly, until one of the participants gets bored or dies. |

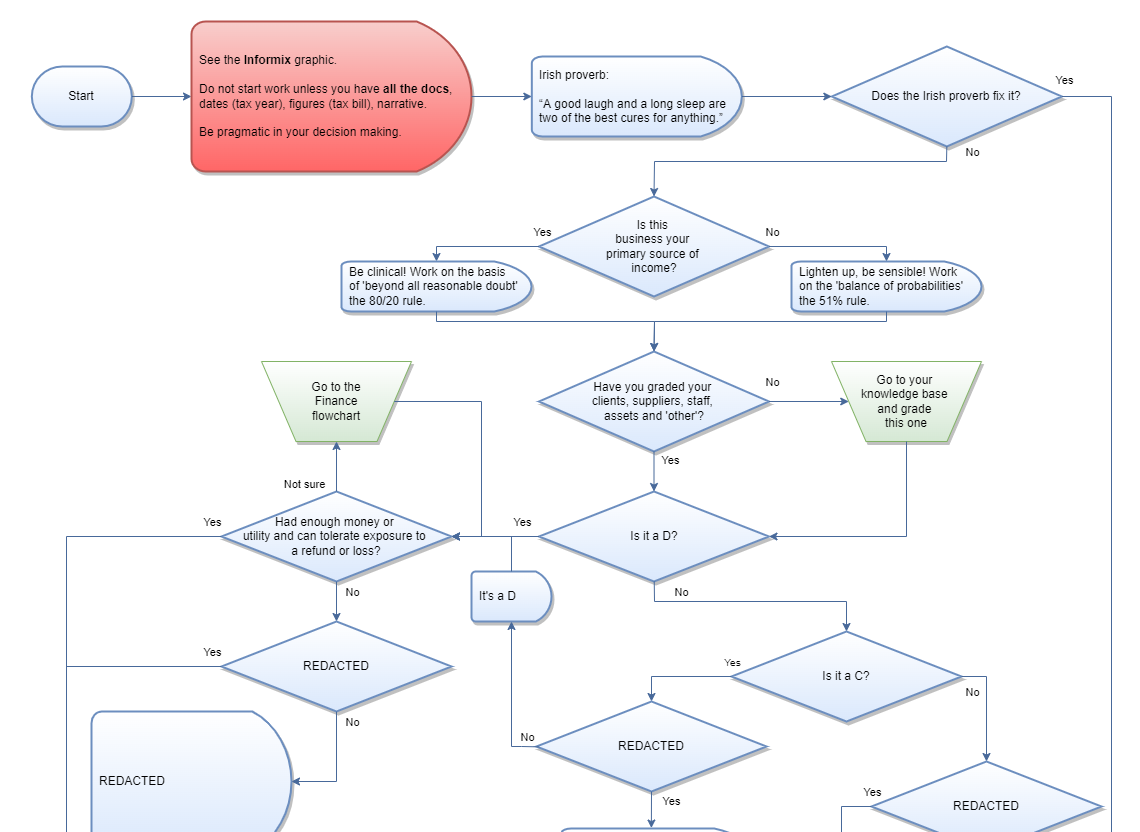

Assuming that you now have adequate information, do you still need to use the UPST? If you do, then it guides you to your solution. Here is the promised extract of the “business” flowchart. It’s been drafted to help with our internal business affairs, and also to help our coaching clients run their businesses. That explains why some bits have interesting questions, and why some bits are redacted. Note also that all clients are graded from A to D.

Occasionally, you may start with the “Pioneer”, follow a route through one or more additional flowcharts, consult the knowledge base, and learn that there is no ready made solution to help you. You end up at the opposite end of the UPST to the “Pioneer” flowchart and find yourself at the aptly named “Solutioneer” flowchart. Yes, you’ve guessed it! It’s a process that tells you how to build a new process and to either add it to the knowledge base, or modify the flowchart(s), or both.

That’s why the UPST is a constantly evolving set of documents!

Paul is also a business coach. Would your business like a helping hand?

Who wants to pay One Million in tax?

Imagine you have walked into some sort of business seminar, and the presenter starts with the question:

“Who wants to pay One Million in tax?”

And before anybody can reply, immediately answers the question by saying:

“I do!”

What’s going on?

Well, think about it. How much money would you need to earn in order to have a tax bill of one million? And if you were earning that much, do you think you would be troubled by your one million tax bill? Probably not. You’d probably be able to survive on the money that you have left over after the tax is paid. If not, you might in any case have sufficient drive to go out and earn some more money. So that (at some point) you’ll find yourself in the fortunate position of not having to worry about a scarcity of money in spite of your big tax bills.

That’s where you want to be. And how are you going to get there?

What you want to be doing is generating more sales and more profit. You’ll be wasting your time if your primary focus is on getting your tax bill down.

Instead, get your profit up, and face the fact that we all have to pay tax.

How will you increase your sales and your profits? You need a business plan. Here’s some revelationary early thinking on business plans, originally written in antiquated French by Henri Fayol, and translated into equally amusing old fashioned English by Constance Storrs. It’s worth a read both for the advice is gives, and for the way that it gives it.

Fayol recommends that you rewrite your plan annually. His advice still holds good today.

Compiling the annual plan is always a delicate operation and especially lengthy and laborious when done for the first time, but each repetition brings some simplification, and when the plan has become a habit, the toil and difficulties are largely reduced. Conversely the interest it offers increases. The attention demanded for executing the plan, the indispensable comparison between predicted and actual facts, the recognition of mistakes made, and successes attained, the search for means of repeating the one and avoiding the other, all go to make the new plan of work of increasing interest and increasing usefulness.

Also by doing this work, the personnel increases in usefulness from year to year, and at the end is considerably superior to what it was in the beginning. In truth, this is not due solely to the use of planning, but everything goes together. A well thought out plan is rarely found apart from sound, organisational, command, coordination, and control practices. This management element exerts an influence on all the rest.

Lack of sequence in activity and unwarranted changes of course are dangers constantly threatening businesses without a plan. The slightest contrary wind can turn from its course a boat which is unfitted to resist. When serious happenings occur, regrettable changes of course may be decided upon under the influence of profound but transitory disturbance. Only a program carefully pondered at an undisturbed time permits of maintaining a clear view of the future and of concentrating maximum possible intellectual ability and material resources upon the danger.

It is in these difficult moments above all that a plan is necessary. The best of plans cannot anticipate all unexpected occurrences which may arise, but it does include a place for these events and prepare the weapons which may be needed at the moment of being surprised. The plan protects the business not only against undesirable changes of course which may be produced by grave events, but also against those arising simply from changes on the part of higher authority. Also, it protects against deviations, imperceptible at first, which end by deflecting it from its objective.

The timid are tempted to suppress the plan or else whittle it down to nothing in order not to expose themselves to criticism, but it is a bad policy even from the point of view of self interest. Lack of plan, which comprises smooth running, also exposes the manager to infinitely graver charges than that of having to explain away imperfectly executed forecasts.

What does your business plan say? You don’t have a plan?

How does not having a plan help you?

If your focus is on tax reduction, then you’re trying to make the tail wag the dog. The General Anti-Abuse Rule (the GAAR) was introduced more than 10 years ago to counter anything which is not based on sound business principles. Whatever clever wheeze you’re thinking of won’t work. Sound business principles do work.

Artificially manipulating things to get your tax bill down will fall foul of s.207(1) & (2) Finance Act 2013. And the penalties under the GAAR can be as much as 60% of the missing tax, on top of paying the missing tax itself. If you’re a 40% taxpayer that’s like asking to pay 64% instead. For example:

| tax on hidden income | 100 | x | 40% | = | 40.00 |

| penalty on missing tax | 40 | x | 60% | = | 24.00 |

| total | 64.00 |

So, rather than waste time on measures to antagonise the tax man, please spend some time on something which will really make a difference. Would you like to have enough income to not worry about paying tax of one million?

Do not be on fire

Do not be on fire, AKA “getting to grip with things”.

Have you ever cooked anything on a camp fire? And have you ever cooked anything in a microwave oven? They’re basically the same thing, but they do the same thing very differently, and they require vastly different levels of care, skill and maintenance. The microwave oven does the challenging stuff for you. However, handle a camp fire badly and you are going to get burnt, and possibly burn others too. The camp fire also takes time and effort to set up correctly, and to decommission safely.

That’s a useful analogy for what it takes to be a company director, compared to being a regular employee. If you do not comply with the directors’ duties in the Companies Act then (metaphorically) you are going to get burnt. Whereas an employee might only risk a (metaphorical) slap on the wrists.

At Proactive, when we’ve worked with new clients for a number of months, we sometimes have to remind them of their duties and obligations. The email can vary in severity, and it usually starts like this:

“I would be failing in my duty as an accountant if I didn’t tell you this now. And, it’s better that you hear it from me now, rather than hear it from HMRC after a few more years of doing the same thing. Nobody wants to end up in court arguing with HMRC or a supplier or a business partner.”

The middle of the email is tailor made to explain some of the concerns we have as professional accountants. It’s factual, it’s not emotional. And it stresses that we ourselves are company directors who comply with the directors’ duties. Hence, we are complying by telling errant directors that they also need to comply.

Usually this “get a grip” email ends with the standard dialogue below, though it sometimes changes depending on the circumstances:

“Your first duty is to act in the best interests of the company and for the benefit of its stakeholders as a whole. The company bank account is not your personal piggy bank. You and your company are not the same thing. I recommend that you read about directors’ duties in sections 170 – 177 of The Companies Act 2006

http://www.legislation.gov.uk/ukpga/2006/46/contents

Please look closely at s172.1(c) and 172.1(e).

Where s.173 says “independent judgment” it means that you need to step away from the business and look at it from the outside as an independent observer. As this mythical independent observer, do you think that the interaction between the company (one legal entity) and the director (a separate legal entity) all comply with s.172.1(e) where is says “maintain a reputation for high standards of business conduct”?

Take the weekend to think this all through, it’s time to get a grip on being a business director, and then let me know what would be a good next step.”

So if you’re leaving the world of employment to work as a contractor through your own limited company, it’s not as straight forward as operating a microwave oven. It’s more like cooking on a camp fire. It’s not a walk in the park, it’s a fire, and you are legally required to get a grip!

Engineers and software developers will know about rule zero . . .

Rule 0 – Do not be on fire!

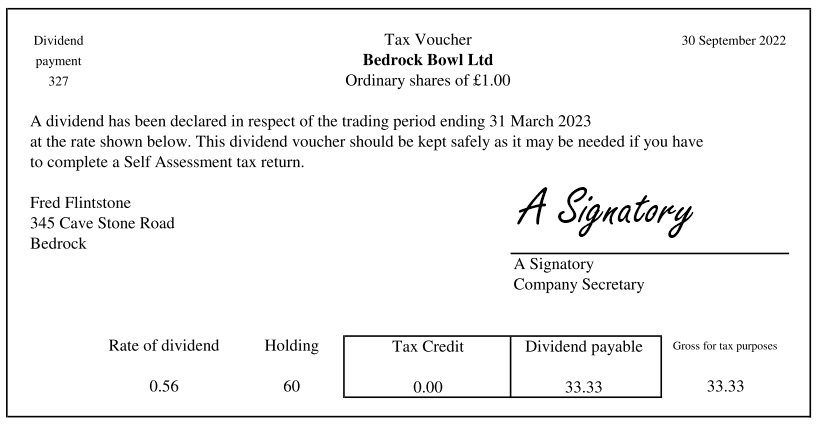

Why are Dividend Vouchers Important?

A dividend voucher is a document given to shareholders of a business when the company declares a dividend to be paid out. They serve as evidence of payment and are also important for those completing self-assessment tax returns.

example dividend voucher – the appearance can vary

How does it work?

Officially a shareholders’ resolution is needed “to declare” a dividend, and a directors’ meeting is needed to establish when “to pay” a dividend. The shareholder and directors meetings can be one and the same meeting and the resolutions and decisions are recorded in the minutes of the meeting.

When a company declares a dividend, and it’s been formalised by the board, dividend vouchers can be prepared and sent to all those who will receive a payment.

The voucher normally includes the trading year it relates to, and is dated (at the top right) with the date it was paid. It states the share class it was declared on and, most importantly, the amount that was paid. The dividend may include a tax credit or a notional tax credit. Whether is does depends on tax law, and that can change from year to year.

This voucher is a shareholder’s evidence of a dividend payment, and they should retain it in their own records. This is particularly important for people who complete a self-assessment tax return, as they would need to declare dividend income on their return. Having a dividend voucher is an easy way of recalling the payment information. If there is an HMRC enquiry dividend vouchers are used to provide evidence of dividend income. Bank statements provide HMRC with evidence of the payment dates.

Companies are obliged to provided dividend vouchers to their shareholders if they are declared. If they do not do so, HMRC could deem payments out of the business accounts to be salary, and Tax/National Insurance would be due. It is the responsibility of the Company Secretary to produce these documents. If your company has no Company Secretary, and has not appointed a company secretarial bureau to do the work, then it is the responsibility of the Company Director(s) to prepare vouchers.

What should I do next?

Most companies declare dividends on a semi-regular basis (for example, once a month or once a quarter) or on an annual basis. You should decide which of these is best for your business, bearing in mind that dividends may only be declared from distributable profits.

Then, once the dividend has been declared and formalised, you should produce vouchers for each shareholder receiving a dividend payment and have this signed by a director and passed to the shareholders directly. It is recommended that companies also keep a copy of the dividend vouchers on file in case a shareholder needs a replacement copy.

If you have declared dividends in the past and have not produced vouchers, you may want to consider preparing some.

Footnote

A company’s Articles of Association typically set out the process for declaring dividends. The directors are responsible for ensuring that dividend payments are made at the right time. The text below shows Article 30 of the UK’s model articles of association for private companies limited by shares.

The Companies Act 2006 refers to “dividends” using the more expressive term “distributions”. We can treat those words as being interchangeable. For a full guide please see s.829 – s.853 of The Companies Act 2006.

30. Procedure for declaring dividends (1) The company may by ordinary resolution declare dividends, and the directors may decide to pay interim dividends. (2) A dividend must not be declared unless the directors have made a recommendation as to its amount. Such a dividend must not exceed the amount recommended by the directors. (3) No dividend may be declared or paid unless it is in accordance with shareholders’ respective rights. (4) Unless the shareholders’ resolution to declare or directors’ decision to pay a dividend, or the terms on which shares are issued, specify otherwise, it must be paid by reference to each shareholder’s holding of shares on the date of the resolution or decision to declare or pay it. (5) If the company’s share capital is divided into different classes, no interim dividend may be paid on shares carrying deferred or non-preferred rights if, at the time of payment, any preferential dividend is in arrear. (6) The directors may pay at intervals any dividend payable at a fixed rate if it appears to them that the profits available for distribution justify the payment. (7) If the directors act in good faith, they do not incur any liability to the holders of shares conferring preferred rights for any loss they may suffer by the lawful payment of an interim dividend on shares with deferred or non-preferred rights.

Do not use Monzo

In our experience, Monzo is simply the worst bank in the UK. They consistently mix up the IN column and the OUT column on the bank statement. They consistently fail to produce statements for pots.

Then when the account closes you risk losing critical data.

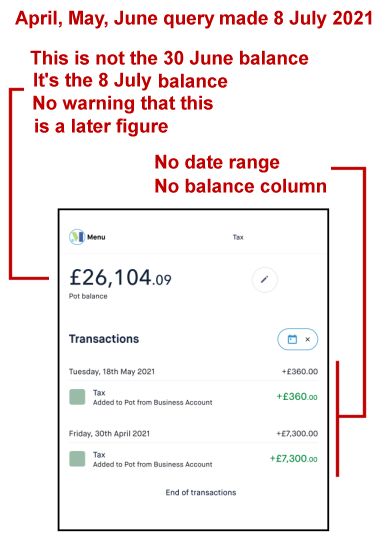

The mobile app, when asked in mid March for a list of all the December transactions will produce a December list with no running balance column. The balance is put at the top of the screen, but it is not the 31 December balance, it is the mid March balance, the one for the date you made the request. If we ask for December figures, we expect the December month end balance to be shown.

Mobile App

To crown it all, today 29 Jul 2022, we have received a second version of a 31 March 2022 bank statement for one single bank account. The month end balance on this second copy of the same statement differs by over £3,000. These two documents cannot both be correct.

PDF statement

Look at the two bank statements in that image. This client had no bank transactions on 29, 30 and 31 March. The statutory accounts are drawn up to 31 March every year. Which figure should be shown in the statutory accounts . . . £14,071.31 or £17,550.25?

In 36 years of accounting work, during which literally thousands of bank statements have passed through our hands, we have never before seen a UK bank provide two copies of the same statement, but with different figures!

Do not use Monzo, they are worse than useless. They may be giving you data which is demonstrably incorrect. These are not the standards expected of a reasonably competent bank.

What does “reasonably competent” mean? Please see the common law of Tort, and dozens of stated cases.

Footnote 1

We had a meeting with Monzo Bank a long time ago, on 17 Dec 2019, to discuss inconsistencies. Nothing changed.

Footnote 2

When you close a business account at Monzo they email you to say that they will provide copies of everything. They do not provide copies of everything!

If you use the business tools with your bank account to generate invoices to your customers, then (before the account closes) you need to manually log in and take a copy of each of those invoices. If you wait until after the account closes you will never get access to this data. When they say “everything” they do not mean “everything”. In any case, you should always (in real time) keep your own copy of every invoice your business ever issues. Do not rely on somebody else to keep it for you. The law requires you to maintain your records and to keep them for 6 years!

Director shareholder payments 2021/22

This is a basic guide to the small salary big dividend method of rewarding yourself from your own company for the tax year ended 5 Apr 2022.

Your company is responsible tor maintaining a corporation tax reserve. Dividends can only be paid from the company’s post tax profit, so that means that the company tax reserve must stay in the company.

If you have no profit, then you can pay no dividend. Take care not to pay dividends out of investor funding or out of bank loans. Investor funding and bank loans are not “profit”.

When most of your income is from dividends then you will need a personal income tax reserve as well. Keep corporate stuff corporate and personal stuff personal. Maintain two tax reserves properly and then you’ll never get a shock when it’s tax payment time.

Follow this system precisely. Ensure bank transactions between your company bank account and your personal bank account follow this system accurately. If it’s not right then HMRC may decide that PAYE tax and National Insurance is due on all of your personal income. You definitely do not want that to happen.

For this process to be legitimate you must be a director/shareholder of a UK limited company.

Your salary is paid to you for the responsibility involved in “holding the office of director” and not for “work done”.

All shareholders must receive dividends in direct proportion to their shareholding.

Beware of adverse consequences if you decide to take 100% of the dividend when you are not the 100% shareholder.

Other than salary, describe these amounts as “drawings” until the overall tax picture for the year is clear. The “dividend” is calculated later. Separate bank transfers are required in order to distinguish salary from drawings. In most cases that means setting up 4 separate payments at end of every calendar month. As Proactive does not hold any authorities on client bank accounts, it’s up to you to make the correct transfers at the correct time.

Basic rate taxpayers

For people whose monthly income does not exceed 4,188.

| Basic rate taxpayers | year ended 5 Apr 2022 |

| Monthly figures | |

| Salary | 736 |

| Primary “Tax Free” drawings (personal allowance) | 311 |

| Secondary “Tax Free” drawings (dividend rate band) | 166 |

| Tertiary drawings (max) liable to 7.5% tax | 2975 |

|

|

|

| Provided always that the monthly income does not total more than | 4188 |

| Put aside 7.5% of your tertiary drawings as a personal tax reserve. | |

Higher rate taxpayers

For people who need (and can afford) monthly incomes between 4,188 and 8,333.

| Higher rate taxpayers – 40% | year ended 5 Apr 2022 |

| Monthly figures | |

| Salary | 736 |

| Primary “Tax Free” drawings (personal allowance) | 311 |

| Secondary “Tax Free” drawings (dividend rate band) | 166 |

| Tertiary drawings liable to 7.5% tax | 2975 |

| Supplementary drawings (max) liable to 32.5% tax | 4145 |

|

|

|

| Provided always that the monthly income does not total more than | 8333 |

| Put aside 7.5% of your tertiary drawings as a personal tax reserve. | |

| Also put aside 32.5% of your supplementary drawings as a personal tax reserve. | |

Top rate taxpayers

For people who need (and can afford) monthly incomes in excess of 8,333.

There are graduated changes for annual incomes between 100,000 and 150,000 and the 45% rate of income tax also kicks in.

| Top rate taxpayers – 45% | year ended 5 Apr 2022 |

| Monthly figures | |

| Salary | 0 |

| Primary “Tax Free” drawings (personal allowance) | 0 |

| Secondary “Tax Free” drawings (dividend rate band) | 166 |

| Tertiary drawings liable to 7.5% tax | 2975 |

| Supplementary drawings liable to 32.5% tax | 5192 |

|

|

|

| Additional drawings liable to 38.1% tax | excess over 8,333.00 |

| Put aside 7.5% of your tertiary drawings as a personal tax reserve. | |

| Also put aside 32.5% of your supplementary drawings as a personal tax reserve. | |

| And put aside 38.1% of your additional drawings as a personal tax reserve. | |

Is this legal?

Yes.

Lord Tomlin stated in the case of IRC vs Duke of Westminster (1936) 19 TC 490 every man is entitled, if he can, to order his affairs so that the tax attaching under the appropriate Acts is less than it otherwise would be.

The key thing is to keep this system in “order” and in compliance with the various Taxes Acts. If you deviate from the guidance above then you may find that your tax planning is not legal.

How much can I draw?

Director/shareholders of UK limited companies tend to reward themselves will a small salary and a dividend. The recommended system for 2024/25 is set out here.

However, in order to get the calculations absolutely right you need to know how much profit the company has, and you probably won’t know that until after the year end accounts have been done. So, part way through a trading year we don’t call these figures “dividends” and we suggest that you take “drawings” in the expectation that a dividend can be declared.

As a rule of thumb you can calculate your drawings using this method. It ignores some fine detail of accounting, but it will get you through to the year end.

Set up a separate company bank account for your company to hold its tax reserve. That’s for corporation tax and (if you’re VAT registered it’s also) for VAT. One savings account is enough.

When a client pays you, put aside 20% of that fee as a provision for corporation tax. Also put aside all of the VAT you charged on that invoice. OK, that ignores allowable expenses and things, and it will be a little too much, but it’s better to have too much tax reserve than too little.

What are you left with, net of corporation tax and net of VAT? Maybe knock off something for expenses as well. Then you have some idea of what the company can afford from its “distributable” profits.

Use that notional figure, and that’s the maximum drawings you can take.

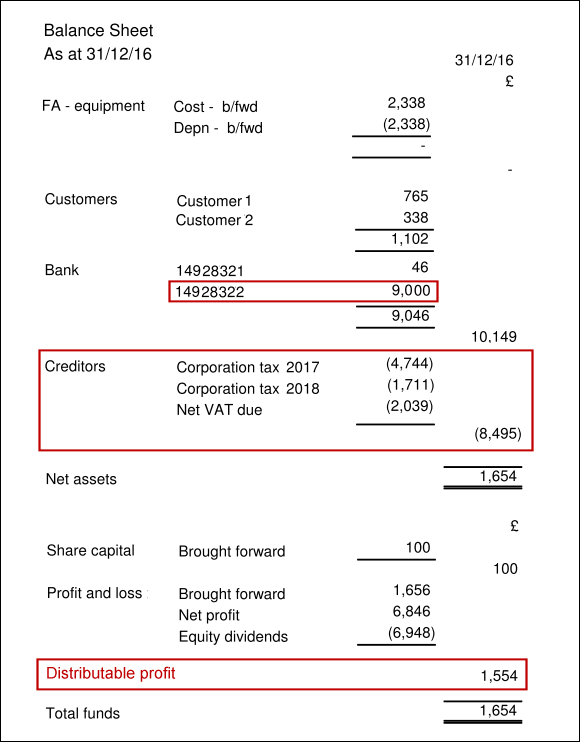

At the end of each quarter, when the bookkeeping reports (and the VAT reports) are done, have a look at your balance sheet. It shows you a forecast of the corporation tax (and the VAT), along with the bank balances on that quarter end date.

In the example above, the tax reserve (in bank account number 2) is £9,000 and that’s £505 more than the total tax forecast of £8,495. This is a good thing.

To the extent that your savings account balance (on the quarter end date) exceeds your creditors balance (on the quarter end date), then you have over provided for tax. If you want to, you can take that excess and move it back to the current account to employ the funds usefully in the business. Or if it’s the other way around, please take steps to restore your tax reserve to its rightful level.

Over time, you might want to adjust that 20% rule down to 19% or 18%. It will take several quarters before you get a feel for what is the right percentage in the case of your own company, and it will depend on having like for like activity each quarter. You’ll know when you hit the right percentage when, every quarter, the excess/deficit on the savings account is consistently small enough to make little difference.

As long as your name does not already appear under “creditors”, then the balance sheet may also show you what the maximum available amount of “distributable” profit is. Assuming that a director’s name does not feature on the balance sheet, then the example above shows that £1,554 is available. That’s just above the bottom line “total funds” figure, and it’s what the company is worth once you ignore the “share capital” line.

If your name is in the “creditors” block then a bit more arithmetic is needed. Firstly, don’t be in that territory on the quarter end date, and secondly, ask your accountant to tell you where you actually stand.

Please do not draw out more than the company can afford. If you do, then HMRC will seek retribution, and they will seek seriously penal levels of tax. We will tell you every quarter when you’re in the danger zone.

7 Habits

The article about Covey and Duncan is here.

I have too much profit, what can I do about it?

This is a fantastic question and we hear it from time to time:

“I have too much profit, what can I do about it?”

It is however a coded version of something else, and it can mean either:

• I don’t have enough profit. I know that, because I have drawn all the money out of my business and I have nothing left to pay my tax bill (and so you must magically engineer a smaller profit for me and a smaller tax bill)!

• I have ridiculously large sums of money floating around, even after paying all my tax bills, I have the home of my dreams, the car of my dreams and I fly everywhere first class, and now I’m in danger of taking up a ridiculously expensive hobby like round-the-world yacht racing!

Depending on which of those statements is the closer to the truth, then the solution is either:

• Make more profit and manage your tax reserve on a weekly or monthly basis. In the short term, borrow some money so that you can pay your tax bill. See Zopa for more details of how you can borrow modest amounts of cash at reasonable rates. We are not in the business of engineering false sets of accounts.

• Become a business angel and invest! There are entry level ways of doing this, even if the pool of cash is as low as £1,000. See Zopa for more details of how you can become an ultra cautious business angel.

If you would like to make more profit, then you need good business advice. Call us and ask about business coaching – we will start by asking you for a copy of your business plan.

Or you can start by looking at Don’t Read My Blog.