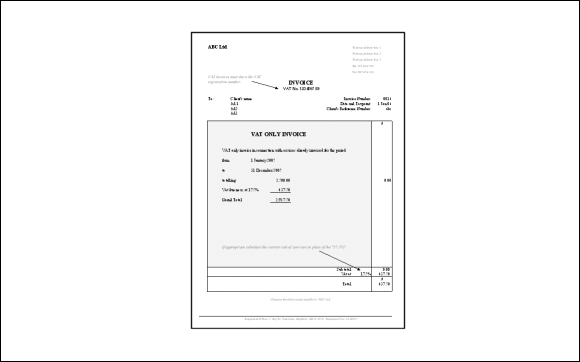

Sometimes an application for VAT registration can be delayed, and you end up completing work after the VAT start date you asked for, but before the VAT number is known.

You cannot charge VAT to a customer until you have your certificate of VAT registration and you know the VAT number.

If you can delay your first invoices then that’s easier, but you may want to invoice in order to collect the fees first, and to collect the VAT later. You should keep you customer informed of this dilemma.

In situations like these, it becomes necessary to issue a later “VAT only” invoice as soon as the VAT number is known.

There are several examples of invoices on this Excel file and the final one shows you how to set out a “VAT only” invoice.

When sending it to the customer it’s best to remind them that you are simply following the HMRC rules. You have a legal duty to do it this way and they have a legal duty to pay you the VAT!

This report was published, in good faith, based on the prevailing information, at 1.00pm on 23 Mar 2020. The situation is changing on a daily basis and any updates to this report will be clearly marked with a date time stamp.

The Government measures are designed to target employees and businesses which are directly affected by the Covid-19 issue. We can argue that we are all affected, but having had dealings with HMRC for 35+ years they can be tricky, and so we suggest that you keep evidence in case you need to (at a later date) show how you have been affected. That includes:

• Medical correspondence for those worst affected.

• Employer correspondence for those laid off.

• Business correspondence for those who experience a downturn.

Do not routinely delete those emails. If somebody cancels a piece of work (or worse) please keep a copy of that email for 6 years beyond the end of your trading year (or tax year).

VAT Registered Taxpayers

VAT due for quarters ended 29 Feb 2020 through to 30 Jun 2020 inclusive will not become due until 7 Aug 2020 at the earliest. This right is automatic and (Government says) no action needs to be taken. If you have VAT to pay, you can pay it on your normal due date if you wish, or hold on to the cash and pay on 7 Aug 2020. No interest will be charged. If you are due a VAT repayment these will be processed as normal.

If you pay quarterly VAT by Direct Debit and want to delay your payments then we recommend cancelling the Direct Debit now. We know from experience (foot-and-mouth disease in 2001 and the farming sector) that “this right is automatic” may not be enough to stop HMRC Direct Debit collections.

Apparently a further announcement is to be made which will allow accumulated VAT debts to be paid over time, and you are to be given until 5 Apr 2021 to bring things up to date.

Irrespective of actual payment dates, VAT returns must still be submitted within the correct time frames.

Mainstream Businesses

Most of the best measures that have been announced are contingent on you being a mainstream business, that is to say, one which:

• has commercial premises subject to business rates; and

• is eligible for either Small Business Rate Relief or Rural Rate Relief.

In these cases you will qualify for grants of up to £10,000 (originally the announcement was £3,000). Whichever local authority deals with your business rates will be in contact you and will automatically initiate the process for you.

All Businesses

Loan scheme – talk to your bank. The Government has agreed to underwrite 80% of any loan capital advanced by your bank under these emergency measures. Theoretically that makes you a lesser risk today that you were a few weeks ago. However, nothing really changes between you and the bank, your application still needs to be well founded and your repayments need to be affordable. The protection is for the bank in case your business goes bankrupt.

Employers and Employees

The Chancellor announced a new a grant from HMRC to employers to cover furloughed workers and keep people on payroll rather than laying them off. The coronavirus job retention scheme would pay up to 80% of employees’ salary to a maximum of £2,500 a month.

The job retention scheme will be backdated to 1 March, with no limit on the amount of funding, and The Chancellor stated that it will be open initially for “at least three months” but didn’t take off the table the option to extend the scheme for longer if necessary.

HMRC will implement a process to fund employers. However, HMRC is in the business of collecting tax and has less experience of handing out grants. The infrastructure to do this is currently a work in progress. Nobody knows when the first grants will be paid.

27 Mar 2019 12.30pm Update – strike out this heading – Self Employed Trade or Partnership

27 Mar 2019 12.30pm Update – new heading – All Self Assessment Cases

Self assessment tax instalments due on 31 Jul 2020 have been postponed, without interest etc, and will now become due on 31 Jan 2021. This is automatic and no action needs to be taken.

27 Mar 2019 12.30pm Update – strike out this para – Apparently you need to be in a self employed trade or be a partner in a traditional partnership to take advantage of this. That means (until we hear otherwise) that self assessment tax instalments due on 31 Jul 2020 on account of your rental income or dividend income, etc, are still due.

Freelance Limited Company

Other than claiming the 80% job retention scheme figure (see “employers” above) there are no specific provisions for small freelance limited companies.

27 Mar 2020 12.30pm update – even the eligibility for this 80% has been questioned by some legal experts. Please see this newer blogpost.

The Government is still addressing this issue and has called for submissions to made by 5pm GMT on 23 Mar 2020.

This telephone number has been rebranded as the Coronavirus Helpline. It’s not a new service as some claim. It has been in existence for many years and is also known as the Business Support Helpline. As far as we know, it is mainly of use to taxpayers who wanted to negotiate “time to pay” arrangements.

AWS operates globally and has set up a branch in the UK for VAT purposes.

Actually, AWS has branches in 18 countries across Europe, so the applicable VAT rules for you, depend on both you and AWS having your “local” place of business in the same EU country. If you are a UK business and you need to obtain a UK VAT receipt from AWS then use the link below. Log in to your AWS account, select the appropriate month and click on the Tax Invoices drop down menu.

The VAT Flat Rate Scheme changes from 1 Apr 2017 when new rules come into force in a heavy handed attempt to combat abuse of the system. The FRS differs from standard VAT accounting because you pay a percentage of your business turnover rather than paying the actual VAT arising on the difference between sales and purchases.

You continue to charge clients the headline rate of 20% VAT and you can potentially benefit by remitting a smaller percentage to the taxman. The FRS rates differ from sector to sector, but for IT contractors the norm used to be a rate of 14.5%. That’s changing to 16.5%.

Generally speaking, the new rules are awful! If you want to see what HMRC said about this (in Nov 2016) the press release and draft legislation are here.

Let’s consider three examples of a software developer with net annual sales of £50,000 and net VATable costs of £5,000.

Standard VAT

accounting

Old FRS Rules

2002 – 2017

New FRS Rules

2017 et seq

Sales

50,000.00

50,000.00

50,000.00

VAT

10,000.00

10,000.00

10,000.00

Total

60,000.00

60,000.00

60,000.00

Gross sales

60,000.00

60,000.00

VAT Flat rate

14.5%

16.5%

VATable costs

5,000.00

VAT

1,000.00

Total

6,000.00

VAT in

10,000.00

VAT out

(1,000.00)

HMRC remittance

9,000.00

8,700.00

9,900.00

“Standard” variation

NIL

£300 better off

£900 worse off

Double those annual sales to £100,000 (some of our clients operate at that level) and you can see that the difference could be either £600 better off or £1,800 worse off.

And do the sums the other way around, under the new FRS rules the VAT of £9,900 represents a rate of 19.8% on the sales of £50,000. That’s a bit like saying “pay all the VAT to HMRC and claim back practically nothing”. This makes the new Flat Rate Scheme nigh on useless!

You may suggest that the software developer in the example should simply deregister because the sales of £50,000 are below the VAT registration threshold of £83,000. Yes, that’s true. And then the VAT recovered would be NIL (instead of getting £1,000 back) and so the business would still be worse off, but to a greater extent!

Wiggle Room

There is not much wiggle room, unless you incur a reasonable amount of cost on “relevant goods”. The new rules are designed to impair only “limited costs” traders. That’s nearly everyone! However, try out the formula below to see if you can escape being labelled as a “limited costs” trader. This calculation has to be done every VAT quarter (so you may find that you alternate between FRS Old Rules and FRS New Rules).

The Formula

Work out your total for VAT inclusive sales.

Calculate a figure for 2% of your VAT inclusive sales.

Work out your total for VAT inclusive costs on “relevant goods”. Goods are tangible things, so be sure to ignore costs for services like office rent, freelance workers, accountants, insurance, travel, telephone calls, etc.

For the purposes of the VAT FRS rules (unless you’re a retailer of these goods) the expression “relevant goods” excludes the following:

Items of a capital nature

Cars

Computers

Printers

Scanners

Mobile phones

Furniture, etc

Fuel for motor vehicles

Spare parts for motor vehicles

Food

Drink

Anything which has a dual personal/business use (like bicycles and parts for their upkeep)

Question 1

Is your expenditure on “relevant goods” less than £250?

Yes > the new FRS rules apply > use a rate of 16.5%

No > go to Question 2

Question 2

Is your expenditure on “relevant goods” less than 2% of your VAT inclusive sales?

Yes > the new FRS rules apply > use a rate of 16.5%

No > the old FRS rules apply > use the old rate from the table of approved rates

Conclusion

If you spend more than £250 (or more than 2% of your VAT inclusive sales – whichever is the greater) every quarter, on . . .

pencils

envelopes

toner cartridges

traditional books and magazines

. . . then you may be in with a chance. In any case, you will have to give your bookkeeper a full analysis of all the goods you buy as “stuff from Amazon for £39” is not enough to tell us if these are “relevant goods”.

In a few cases, where you’re on a really low flat rate (teachers and trainers are on a 12% flat rate under the old rules) it might be worthwhile buying a few toner cartridges every quarter and then chucking them in a cupboard until you retire from business. You might then pass the test “more than 2% of your VAT inclusive sales” and you would still get your old flat rate. This has to be assessed on a case by case basis, but I have at least one lecturer who makes so much bounty on the 12% flat rate that it’s worth his while using some of that bounty to buy “relevant goods” which will languish unused, and he will still win overall!

In all other cases, we recommend leaving the Flat Rate Scheme on 31 Mar 2017 and adopting the standard approach to VAT from 1 Apr 2017. We are writing to all affected clients with a proforma letter which needs a real ink signature and which needs to be returned to us by 28 Feb 2017 so that we can get it submitted, agreed by HMRC, and implemented at midnight on 31 Mar 2017.

A withdrawal from the Flat Rate Scheme does not change the way that you bill your clients. If you’re company is VAT regsitered then it will still be VAT registered, and we will look after your VAT for you using the standard method and not the flat rate method.

Lastly

Beware of trying to fiddle the system. Any attempt to invoice in advance for services to be provided on or after 1 April 2017, to capture that invoice within the old FRS rates, will be treated as if the invoice was issued on 1 April 2017 (paras 8.2 and 9.7 of VAT notice 733).

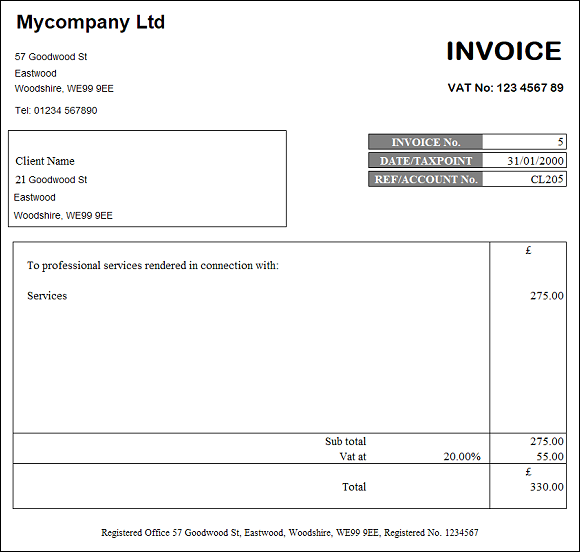

All invoices must show the same information as your letter headed paper, business address, registered number and that sort of thing (to comply with The Companies Act 2006). The following rules also apply:

The word “Invoice” must appear and be abundantly clear.

Invoices must be sequentially numbered and the numbering must be purely numeric.

The date of the invoice must be shown, along with the word “taxpoint”.

The name and address of the person being invoiced must appear. This is the name of your customer and not the name of the individual in their head office. If your customer is a business called XYZ Trading Ltd then the invoice should be addressed to XYZ Trading Ltd. You can for example also mark the invoice “F.A.O. Mr Jones” if you wish, but if you address it directly to Mr Jones then (in law) it looks like your are charging the fee to Mr Jones and making him personally liable for the debt.

If your UK business is VAT registered, the invoice must show a proper analysis of how the VAT has been calculated. A sub-total row, followed by a VAT calculation row which includes both the applicable VAT rate and the VAT payable, and finally a total row.

VAT invoices must show your VAT registration number.

VAT invoices to all UK customers must charge VAT at the current standard rate. There are a very few limited exceptions to this rule – talk to us if you sell “advertising space” to registered charities.

If you sell downloadable eServices from your website please read about VATMOSS first and then come back and read this! Normally, VAT invoices to EU customers (for services) must charge VAT at the current standard rate (as of 4 Jan 2011 that’s 20%) unless that customer is VAT registered in their State of origin.

This item relates only to invoices for work done before 1 Jan 2021 – it is here (in italics) just in case you are working on older records. VAT invoices (for intellectual services) to VAT registered businesses in the other 27 EU States must show the customer’s VAT number (usually below their address) and charge VAT at a special rate of 0%. The phrase “intellectual services” means the services of people like accountants, lawyers, teachers etc where what you are paying for is primarily knowledge and/or skill. It may or may not include advertising and sponsorship, and conferences and catering, when any of these services are performed in the UK. Talk to us if this applies to you.

This item relates only to invoices for work done before 1 Jan 2021 – it is here (in italics) just in case you are working on older records. If you cannot verify the VAT number of your EU customer on the Europa website then you must assume that they are not VAT registered and that means charging them 20% VAT!

VAT invoices to customers outside the UK vary depending on what you supplied and where you supplied it. If you supply intellectual services to a non-UK customer then the services are “outside the scope” of VAT and the VAT calculation row on the invoice should simply state “outside the scope”. In all other cases you may want to check the “place of supply” rules with us, and the meaning of “intellectual services” before you invoice your non-UK customer.

VAT invoices must be in GB Pounds. If you wish, you can show a different currency in the narrative within the “description of product/service”. It has to be done like this to comply with Reg 14(1)(i) The Value Added Tax Regulations 1995 and that allows VAT officers to quickly identify the right figures when they carry out a records inspection. If your client objects tell them you have to do it in GBP and the law is set out here.

Your policy on preparing currency conversions must have a reasonable basis, and be consistent each time. Our policy is to use average monthly rates as per the HMRC published figures and that way there is never any dispute over the authenticity.

You cannot charge VAT to clients until your VAT registration is confirmed. If in doubt, please consult your accountant before charging anybody VAT.

If you are in the habit of billing your clients with local currency figures in your narrative, then you will get used to the fact that the remittance you receive is normally less than the amount you invoiced. You may want to bear this is mind when generating your invoices so that you can figure in a little extra for bank charges and exchange rate losses.

When you pass your records to the bookkeeper, we will check for bank charges and exchange rate losses (or gains). If the bank charges are clearly shown, then we will record them as such. If that still leaves a small exchange rate loss (or gain) the we will record that separately as an allowable expense (or other income) and so your business will be taxed correctly on the amount that it has actually received. There is no need to for you to prepare any other documentation to show the loss (or gain) and we will calculate it using the monthly exchange rates published by HMRC.

Your invoice to your foreign client should fit one of these three examples.

Example 1 of 4

This example relates only to invoices for work done before 1 Jan 2021 – it is here just in case you are working on older records Non UK client in the EU with an EU VAT number

Example 2 of 4

This example relates only to invoices for work done before 1 Jan 2021 – it is here just in case you are working on older records Non UK client in the EU without an EU VAT number

All businesses need standardised documents for their correspondence and invoices. An invoice is basically a standard letterhead with the addition of a number of billing points. The examples set out here assume that your business is a limited company.

VAT invoices must show:

Your address and the address of your company registered office. If your company registered office and your principal place of business are one and the same, you only need to show the address once, provided that it is clear that they are one and the same!

Your company registration number.

Your VAT registration number.

The date of the invoice.

The invoice number. Invoices must be sequentially numbered, using a plain and simple, and purely numeric system. Do not skip numbers. Invoices must run in number order and also in date order. Do not use a number on draft invoices if that results in the sequence becoming broken. Draft invoices should only be given a number when they are finalised and issued.

The name and address of the person being invoiced. This is the name of your client and not necessarily the name of the individual who works there. You can for example mark the invoice “F.A.O. Mr Jones”, but it should be addressed to the client, for example “London Time Machines Ltd”.

The amounts in GB Pounds. If you wish, you can show a different currency within the dialogue within the invoice, but not where it’s likely to confuse a VAT officer. In the event of a records inspection, the VAT officer must be able to clearly see the GBP figures, and especially the ones at the foot of the invoice.

A sub total line, showing the net figure excluding the VAT.

A VAT line, showing the applicable rate and the VAT amount in isolation.

A total line, showing the sum of the net amount and the VAT.

Once an invoice has been issued to a client, it should never be amended. If there is anything wrong with an invoice the correction must be done in the way we have set out here https://www.proactive.ly/news/?p=353

I’ve only just registered my business. Can I claim pre-trade expenses which I’ve paid for personally? And can I claim back old VAT?

The short answer is “it depends”.

The basic principal is that “if you paid for something in the knowledge that you were starting a business, and the prime motive for buying this something was to enhance that business, then it is a business expense” and you can normally claim for it. That applies to both goods and services, and in order to claim the full cost you must satisfy both parts of this test, that (a) there was a business prime motive and (b) the purchase was within the three years preceding day one of the business.

Alternatively, if (for example) you bought your desktop computer and printer four years ago, and you introduced them into the business on day one, then you can claim their “fair market value” on day one as an allowable expense. This applies to goods only. If you cannot claim them under the three year rule mentioned above, then claim them under the fair market value rule, and use eBay or GumTree to work out what a fair market value for your something is. You can also claim for (for example) a CamCorder which you bought for the family two years ago, but then introduced into the business – it may fail the “business prime motive” test at the date of purchase, but it could still qualify under the “fair market value” rule as long as it is now a business asset and is not a family asset!

In either case, you need to submit a claim form to your business and have the precise amount reimbursed from the business account to your personal account. This applies, even if you are the only director/employee/worker. Documentation and adequate evidence are required in support of all claims.

If you’re thinking of introducing your car into your new limited company, you probably shouldn’t. The costs of tax and national insurance, on the benefit in kind of having a company car, usually mean that it’s actually more cost effective to run the car personally and to claim a business mileage allowance from your company.

Before doing the claim form, any VAT registered businesses should consider these additional rules. You can claim for the VAT on goods (and in limited circumstances on services too) provided that they:

• were purchased within the three years preceding the date of your VAT registration

• are still in the possession of the business on the date of your VAT registration

• are actually used in the course of the business; and

• satisfy the business prime motive test

Note that three years preceding the date of your VAT registration is only the same as three years preceding the commencement of the business if you were VAT registered from day one. There’s a subtle difference for businesses which waited a few months (or a few years) before applying for their VAT registration!

There are further guides on this site which may help you:

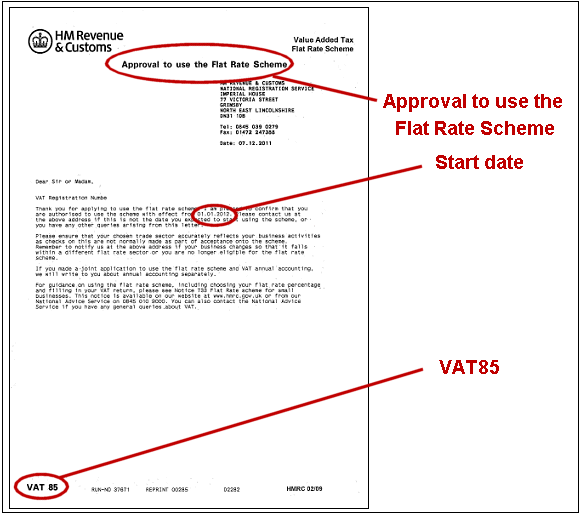

After your FRS application is approved you should receive a confirmation letter like this one.

As soon as you get that please let us have copy so that we can make sure our systems are up to date and we help you to get the next VAT return in, with the right amount, and on time!

HMRC first introduced digital processes in 2007 and (as at 1 Jan 2021) has not yet abandoned the use of paper. Some things are only set out on paper, like a VAT reporting cycle!

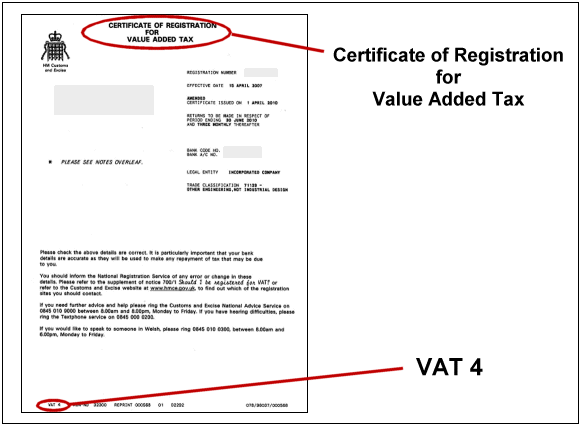

That means that we need a copy of your VAT Registration Certificate. A form VAT4. HMRC normally posts this about 7-14 days after registration.

It looks a bit like this example and (amongst other things) it tells us if you have a March, June, September, December reporting cycle or some other pattern.

There is little logic in VAT legislation, and so the system is set out here for your information. Whether we like it or not, we have to follow the rules!

If you are VAT registered, then you charge VAT to your clients, on top of the cost of your product or services.

If in the course of doing that you incur expenses and you want to recharge those expenses, then you have to charge VAT on top of the expenses as well. The rate is the same rate that you would use for charging VAT on fees (and that can vary). The absurdity of this “VAT on recharged expenses rule” means that (for example) the cost of a train ticket which is normally exempt from VAT, becomes a VATable item the moment you recharge it to a client. The same applies to a postage stamp, or a carton of milk, normally these are non-VAT items, but they become VATable items the moment you recharge them to a client.

Any expense which you “modify” or “process” or “consume” before you recharge it to your client falls into this VAT trap. The only time you can avoid charging VAT on an expense is when it falls into the narrow definition of a “disbursement”.

That’s for things that undergo “no change” as part of your service, but which you pass on intact to your client, or on behalf of your client. In the case a solicitor handling a house purchase, the stamp duty is a disbursement and not an expense. It is not “modified, processed or consumed” as part of the service which the solicitor has provided.

Likewise, if I recharge the costs of providing my clients with tea, coffee and milk, then I need to add VAT to the bill (even though food is not normally subject to VAT). Whereas if I bought a carton of milk for you and handed it over, unused and unopened, then it would be classed as a disbursement.

Crazy, but true. As a general rule add VAT on top of all the expenses that you recharge to your clients!

Please also bear in mind that if you want money from your customer then it is always done on invoice. The expression “expense claim” is something that employers and employees use. On a business to business level you do not claim, you invoice. A full run down of “Invoicing and Sales” is set out at step 2 on this page.