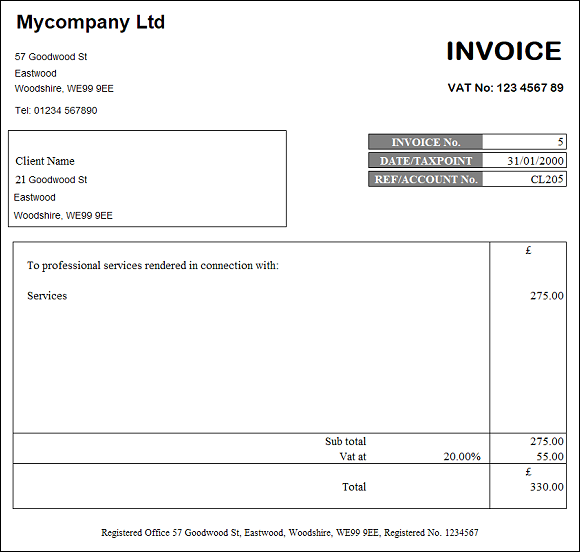

All invoices must show the same information as your letter headed paper, business address, registered number and that sort of thing (to comply with The Companies Act 2006). The following rules also apply:

- The word “Invoice” must appear and be abundantly clear.

- Invoices must be sequentially numbered and the numbering must be purely numeric.

- The date of the invoice must be shown, along with the word “taxpoint”.

- The name and address of the person being invoiced must appear. This is the name of your customer and not the name of the individual in their head office. If your customer is a business called XYZ Trading Ltd then the invoice should be addressed to XYZ Trading Ltd. You can for example also mark the invoice “F.A.O. Mr Jones” if you wish, but if you address it directly to Mr Jones then (in law) it looks like your are charging the fee to Mr Jones and making him personally liable for the debt.

- If your UK business is VAT registered, the invoice must show a proper analysis of how the VAT has been calculated. A sub-total row, followed by a VAT calculation row which includes both the applicable VAT rate and the VAT payable, and finally a total row.

- VAT invoices must show your VAT registration number.

- VAT invoices to all UK customers must charge VAT at the current standard rate. There are a very few limited exceptions to this rule – talk to us if you sell “advertising space” to registered charities.

- If you sell downloadable eServices from your website please read about VATMOSS first and then come back and read this! Normally, VAT invoices to EU customers (for services) must charge VAT at the current standard rate (as of 4 Jan 2011 that’s 20%) unless that customer is VAT registered in their State of origin.

- This item relates only to invoices for work done before 1 Jan 2021 – it is here (in italics) just in case you are working on older records. VAT invoices (for intellectual services) to VAT registered businesses in the other 27 EU States must show the customer’s VAT number (usually below their address) and charge VAT at a special rate of 0%. The phrase “intellectual services” means the services of people like accountants, lawyers, teachers etc where what you are paying for is primarily knowledge and/or skill. It may or may not include advertising and sponsorship, and conferences and catering, when any of these services are performed in the UK. Talk to us if this applies to you.

- This item relates only to invoices for work done before 1 Jan 2021 – it is here (in italics) just in case you are working on older records. If you cannot verify the VAT number of your EU customer on the Europa website then you must assume that they are not VAT registered and that means charging them 20% VAT!

- VAT invoices to customers outside the UK vary depending on what you supplied and where you supplied it. If you supply intellectual services to a non-UK customer then the services are “outside the scope” of VAT and the VAT calculation row on the invoice should simply state “outside the scope”. In all other cases you may want to check the “place of supply” rules with us, and the meaning of “intellectual services” before you invoice your non-UK customer.

- VAT invoices must be in GB Pounds. If you wish, you can show a different currency in the narrative within the “description of product/service”. It has to be done like this to comply with Reg 14(1)(i) The Value Added Tax Regulations 1995 and that allows VAT officers to quickly identify the right figures when they carry out a records inspection. If your client objects tell them you have to do it in GBP and the law is set out here.

- Your policy on preparing currency conversions must have a reasonable basis, and be consistent each time. Our policy is to use average monthly rates as per the HMRC published figures and that way there is never any dispute over the authenticity.

You cannot charge VAT to clients until your VAT registration is confirmed. If in doubt, please consult your accountant before charging anybody VAT.

If you are in the habit of billing your clients with local currency figures in your narrative, then you will get used to the fact that the remittance you receive is normally less than the amount you invoiced. You may want to bear this is mind when generating your invoices so that you can figure in a little extra for bank charges and exchange rate losses.

When you pass your records to the bookkeeper, we will check for bank charges and exchange rate losses (or gains). If the bank charges are clearly shown, then we will record them as such. If that still leaves a small exchange rate loss (or gain) the we will record that separately as an allowable expense (or other income) and so your business will be taxed correctly on the amount that it has actually received. There is no need to for you to prepare any other documentation to show the loss (or gain) and we will calculate it using the monthly exchange rates published by HMRC.

Your invoice to your foreign client should fit one of these three examples.

Example 1 of 4

This example relates only to invoices for work done before 1 Jan 2021 – it is here just in case you are working on older records Non UK client in the EU with an EU VAT number

Example 2 of 4

This example relates only to invoices for work done before 1 Jan 2021 – it is here just in case you are working on older records Non UK client in the EU without an EU VAT number

Example 3 of 4

Non UK client

Example 4 of 4

Standard UK invoice to a UK client