The retained profits generated by UK companies of all sizes can be distributed to shareholders. For professional workers (such as contractors, consultants, and freelancers), dividends make up the bulk of income drawn from small limited companies.

In order to get the calculations absolutely right you need to know how much profit the company has, and you probably won’t know that until after the year end accounts have been done. So, part way through a trading year we don’t call these figures “dividends” and we suggest that you take “drawings” in the expectation that a dividend can be declared.

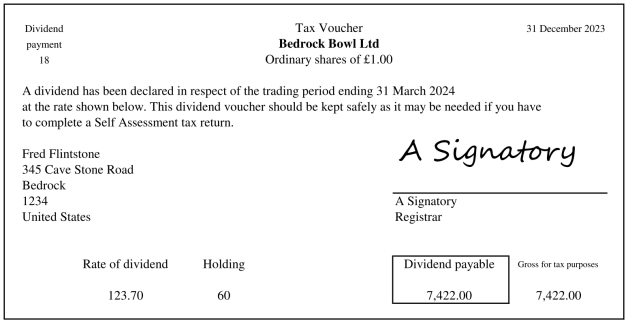

If a limited company has made a profit, it is free to distribute these funds to its shareholders. This is the money the company has remaining after paying all business expenses and liabilities, plus any outstanding taxes (such as Corporation Tax and VAT). Even if the year end has not yet been reached, quarterly dividends might be declared on account of the profit which the company anticipates it will make.

‘Retained profit’ may have been accumulated over a period of time, and any excess profits not distributed as dividends simply remain in the company’s bank account. If you choose to distribute all of the available profit then it is likely that you have 80% of the company profits in your hands, whilst the company keeps 20% as a tax reserve.That’s how it looks from the company’s point of view.

As there is very little logic in tax law, your net dividend (prior to 6 Apr 2016) is deemed to have a 10% notional tax credit attaching to it. From an individual point of view, your net dividend is therefore 90% of some notional gross figure. These are the figures shown on the dividend voucher and these are the figures that go into a personal tax return (up to 5 Apr 2016).

Working via a limited company is a tax efficient way to operate, as National Insurance Contributions (NICs) are not payable on company dividends, whereas they are payable on salaried income.

Dividends must be distributed according to the percentage of company shares owned by each shareholder, i.e. if you own half the company’s shares, you will receive 50% of each dividend distribution.

In order to check how we calculate the dividend figure, our clients are provided with a 488120 ledgers report each quarter. Under the heading Creditor – YourName you can see how we have matched any periodic drawings to the quarterly dividends. This section of the 488120 report may also show idiosyncratic figures, adjusting your dividend for any personal expenditure made on behalf of an individual from a company bank account.