A dividend voucher is a document given to shareholders of a business when the company declares a dividend to be paid out. They serve as evidence of payment and are also important for those completing self-assessment tax returns.

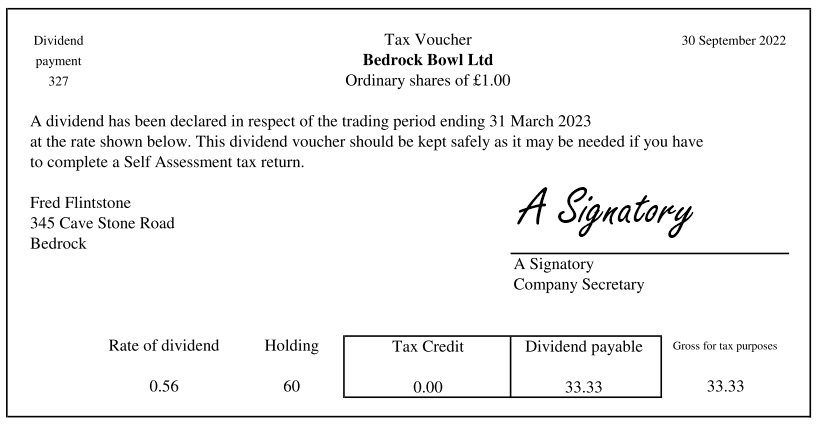

example dividend voucher – the appearance can vary

How does it work?

Officially a shareholders’ resolution is needed “to declare” a dividend, and a directors’ meeting is needed to establish when “to pay” a dividend. The shareholder and directors meetings can be one and the same meeting and the resolutions and decisions are recorded in the minutes of the meeting.

When a company declares a dividend, and it’s been formalised by the board, dividend vouchers can be prepared and sent to all those who will receive a payment.

The voucher normally includes the trading year it relates to, and is dated (at the top right) with the date it was paid. It states the share class it was declared on and, most importantly, the amount that was paid. The dividend may include a tax credit or a notional tax credit. Whether is does depends on tax law, and that can change from year to year.

This voucher is a shareholder’s evidence of a dividend payment, and they should retain it in their own records. This is particularly important for people who complete a self-assessment tax return, as they would need to declare dividend income on their return. Having a dividend voucher is an easy way of recalling the payment information. If there is an HMRC enquiry dividend vouchers are used to provide evidence of dividend income. Bank statements provide HMRC with evidence of the payment dates.

Companies are obliged to provided dividend vouchers to their shareholders if they are declared. If they do not do so, HMRC could deem payments out of the business accounts to be salary, and Tax/National Insurance would be due. It is the responsibility of the Company Secretary to produce these documents. If your company has no Company Secretary, and has not appointed a company secretarial bureau to do the work, then it is the responsibility of the Company Director(s) to prepare vouchers.

What should I do next?

Most companies declare dividends on a semi-regular basis (for example, once a month or once a quarter) or on an annual basis. You should decide which of these is best for your business, bearing in mind that dividends may only be declared from distributable profits.

Then, once the dividend has been declared and formalised, you should produce vouchers for each shareholder receiving a dividend payment and have this signed by a director and passed to the shareholders directly. It is recommended that companies also keep a copy of the dividend vouchers on file in case a shareholder needs a replacement copy.

If you have declared dividends in the past and have not produced vouchers, you may want to consider preparing some.

Footnote

A company’s Articles of Association typically set out the process for declaring dividends. The directors are responsible for ensuring that dividend payments are made at the right time. The text below shows Article 30 of the UK’s model articles of association for private companies limited by shares.

The Companies Act 2006 refers to “dividends” using the more expressive term “distributions”. We can treat those words as being interchangeable. For a full guide please see s.829 – s.853 of The Companies Act 2006.

30. Procedure for declaring dividends (1) The company may by ordinary resolution declare dividends, and the directors may decide to pay interim dividends. (2) A dividend must not be declared unless the directors have made a recommendation as to its amount. Such a dividend must not exceed the amount recommended by the directors. (3) No dividend may be declared or paid unless it is in accordance with shareholders’ respective rights. (4) Unless the shareholders’ resolution to declare or directors’ decision to pay a dividend, or the terms on which shares are issued, specify otherwise, it must be paid by reference to each shareholder’s holding of shares on the date of the resolution or decision to declare or pay it. (5) If the company’s share capital is divided into different classes, no interim dividend may be paid on shares carrying deferred or non-preferred rights if, at the time of payment, any preferential dividend is in arrear. (6) The directors may pay at intervals any dividend payable at a fixed rate if it appears to them that the profits available for distribution justify the payment. (7) If the directors act in good faith, they do not incur any liability to the holders of shares conferring preferred rights for any loss they may suffer by the lawful payment of an interim dividend on shares with deferred or non-preferred rights.